yahoo Press

Invest Your Child’s Future With $3,000: See What It Could Become by Age 18

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

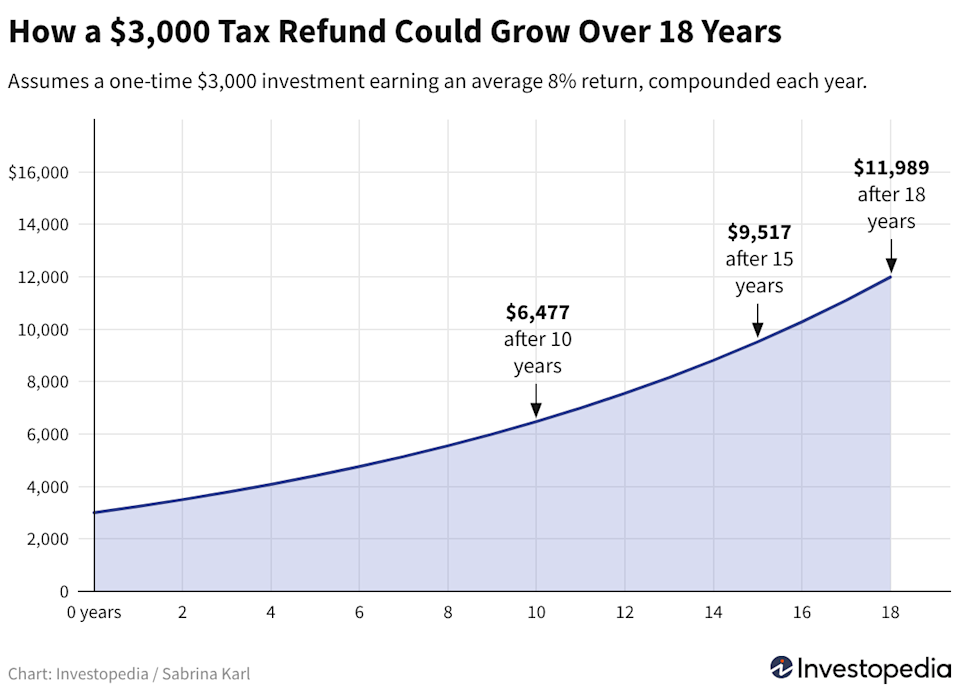

A one-time $3,000 tax refund invested in a 529 plan could grow to about $12,000 in 18 years at an 8% annual return. 529 plans offer tax-free growth when funds are used for qualified education expenses, boosting long-term savings power. While saving for college can be smart, building an emergency fund and paying down high-interest debt should likely come first. If you’ve ever gotten a tax refund, it can feel like free money. It may be tempting to put it toward a vacation or funding a home improvement project—or even just covering the necessities. If you’re able, consider using it for something with lasting effects for both you and your offspring: Start or boost a 529 plan for your child’s future college costs. Opening and regularly funding a 529 college savings plan is a big step toward setting aside money for higher education. Named for a section of the Internal Revenue Code, 529 plans are tax-advantaged savings plans designed specifically for education expenses. For illustration, let’s assume an average 8% annual return, which reflects a stock-heavy portfolio over a long time horizon. If you invested a $3,000 tax refund in a 529 plan and left it untouched, that single contribution could grow to about $12,000 in 18 years. A larger, one-time refund of $5,000 could grow to nearly $20,000 over the same period. Those figures show what a one-time tax refund could grow to in a 529 plan, with no additional contributions. But if you invested that same amount every year, the long-term impact would be far larger, as the chart below shows. In all of these scenarios, remember that the figures are estimates, not guarantees. While 8% may reflect a long-term average return for stock-heavy portfolios, actual results can vary significantly from year to year. While often associated with four-year universities, 529 plans can also cover private K–12 tuition, trade schools, and up to $10,000 in student loan repayment per beneficiary. That added flexibility can make contributing feel less restrictive. One reason a 529 can be so powerful is its tax-free growth. Though the contributions are not tax deductible in all states, the earnings in the account are never taxed if used for qualified education expenses. Here’s how 529s compare with other types of accounts that could be used to save for education: Comparing Accounts and Taxes Where the refund goes Are contributions deductible? Is growth taxed while invested? Is money taxed when withdrawn? 529 plan Usually no (some states say yes)* No No (if used for qualified expenses) UGMA/UTMA custodial account No Yes (subject to kiddie tax rules) No, but gains may be taxable Taxable brokerage account No No Yes (on gains) High-yield savings account No Yes (every year) Already taxed when earned Qualified education expenses include costs tied to traditional college, trade school, and private K–12 tuition. Because earnings in a 529 aren’t taxed when used for those expenses, more of your money can remain invested and compounding over time. If 529 funds aren’t used for qualified education expenses, earnings are subject to income tax and typically a 10% federal penalty. By contrast, custodial and taxable brokerage accounts don’t carry education-use restrictions—but their investment gains may be taxed along the way. If your child doesn’t use all the money in a 529, you may be able to convert up to $35,000 into a Roth IRA for them over time. The 2024 rule change reduces the risk of overfunding and adds a long-term savings benefit. If you expect to face college or other education costs in the future, a 529 can be a powerful way to put your tax refund to work—but only if you’re comfortable leaving the money invested until those expenses arise. Families should also check whether their state offers a tax deduction or credit for 529 contributions, which can further improve the return on your deposit. However, if you have high-interest debt or lack a basic emergency fund, addressing those first can provide more immediate financial stability than starting a college account. If you’re behind on retirement savings, prioritizing that may make more sense. Students can borrow for college, but retirees generally can’t borrow to cover living expenses. Even if your child is only a few years away from needing education funds, a 529 can still help cover near-term costs such as tuition, fees, books, and certain trade-school or career-training programs. The earlier you invest, the more time your refund has to compound—turning what feels like extra cash today into meaningful help when tuition bills arrive. Read the original article on Investopedia