yahoo Press

Small-Cap Oil Producer Hits 50 Consecutive Dividends With a 10.6% Yield, But the Cushion Is Thin

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

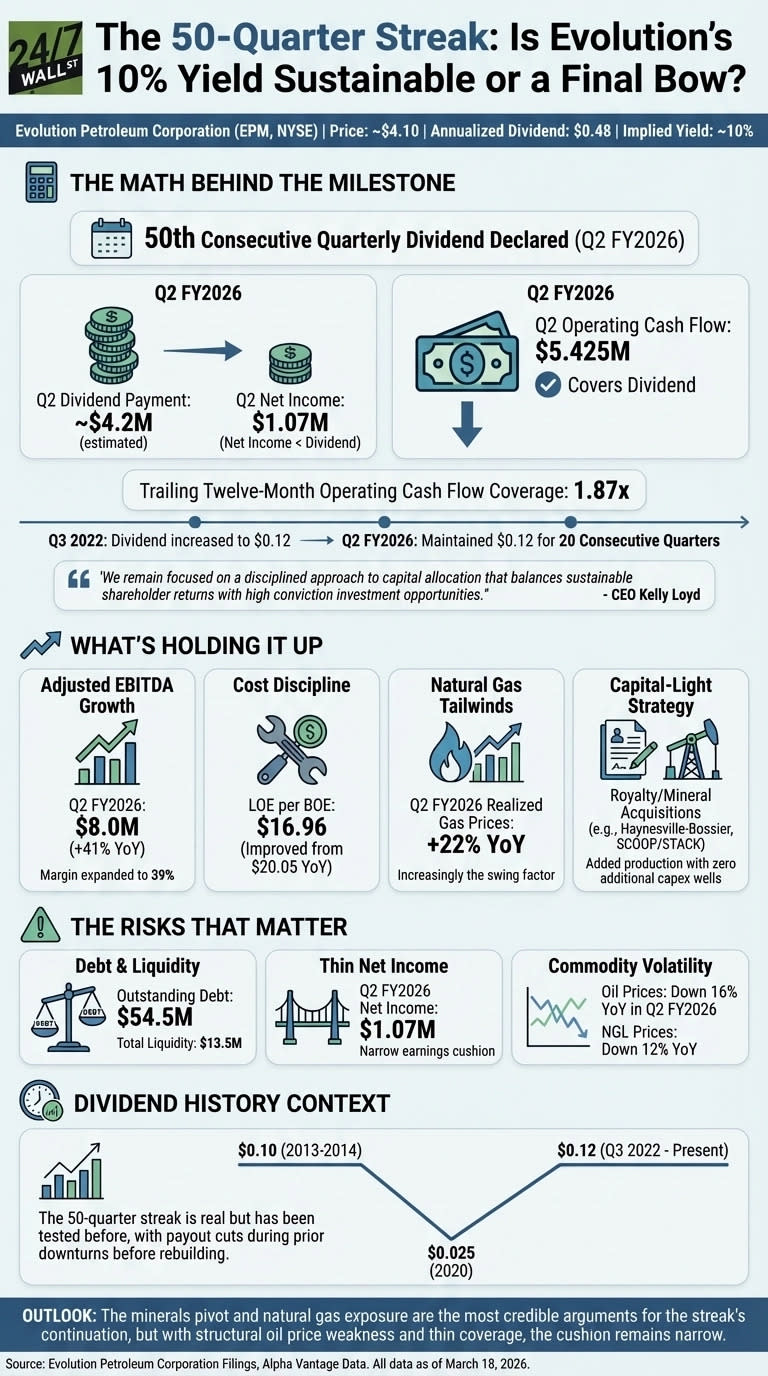

Evolution Petroleum (EPM) maintained its 50th consecutive quarterly dividend at $0.12 per share, yielding 10.5%, despite Q2 net income of only $1.07 million against dividend payments of $4.2 million; adjusted EBITDA grew 41% year-over-year to $8.0 million with lease operating expenses down to $16.96 per BOE, while trailing twelve-month operating cash flow covered dividends 1.87x. Natural gas tailwinds and a shift toward capital-light minerals and royalty acquisitions are sustaining Evolution’s dividend payout, but structural oil price weakness, $54.5 million in debt against only $13.5 million in liquidity, and a thin earnings cushion expose the streak to commodity volatility. If you're focused on picking the right stocks and ETFs you may be missing the bigger picture: retirement income. That is exactly what The Definitive Guide to Retirement Income was created to solve, and it's free today. Read more here Founded in 2003, Evolution Petroleum (NYSE:EPM) is focused on developing and producing onshore oil and natural gas properties in the US and just declared its 50th consecutive quarterly dividend, a milestone that puts it in rare company among small-cap energy producers. With the stock at $4.48 and the annualized payout at $0.48 per share, the implied yield is roughly 10.6% - nearly 577 basis points above the 10-year Treasury at 4.28%, and this spread demands scrutiny. In Q2 FY2026 (ending December 2025), Evolution Petroleum reported net income of $1.1 million and paid $4.2 million in dividends. Operating cash flow of $5.425 million covered the dividend payment for the quarter. The company has maintained $0.12 per share every quarter since Q3 2022, never wavering even through net losses. This infographic analyzes Evolution Petroleum's (EPM) financial performance to assess the sustainability of its 50-consecutive quarterly dividend streak and 10% yield. It details the company's Q2 FY2026 metrics, supporting factors, and significant risks impacting dividend coverage. Have You read The New Report Shaking Up Retirement Plans? Americans are answering three questions and many are realizing they can retire earlier than expected. CEO Kelly Loyd framed the outlook on the Q2 call: "We remain focused on a disciplined approach to capital allocation that balances sustainable shareholder returns with high conviction investment opportunities." The headline earnings figure understates cash generation. Adjusted EBITDA jumped 41% year-over-year to $8.0 million, with margins expanding to 39% from 28% the prior year. Lease operating expenses fell to $16.96 per BOE from $20.05, reflecting genuine cost discipline. On a trailing twelve-month basis, operating cash flow covered dividends at 1.87x. Natural gas is increasingly the swing factor, as Henry Hub prices spiked to $7.72 in January 2026 before retreating to $3.62 in February, and Evolution's realized natural gas prices rose 22% year-over-year in Q2. WTI crude sat at $64.51 in February 2026, well below the $75.74 seen in January 2025. Evolution has also been pivoting toward capital-light minerals and royalty acquisitions. Four Haynesville-Bossier deals totaling roughly $4.5 million added production with no incremental lifting costs. Loyd noted that "when oil prices are low, it presents compelling M&A opportunities rather than drilling opportunities." Outstanding debt stands at $54.5 million, while total liquidity is only $13.5 million. The stock has rallied 30.14% year-to-date from $3.45 at year-end 2025, compressing the yield from even higher levels. Three of four analysts covering the stock rate it a Buy, with a consensus price target of $5.06. Evolution cut the payout from $0.10 in 2014 to $0.025 by mid-2020 during prior commodity downturns, then rebuilt it. The 50-quarter streak is real but has been tested before, and with oil prices structurally weaker and Q2 operating cash flow covering the dividend by a thin margin, the cushion is narrow. The minerals pivot and natural gas exposure are the most credible arguments this streak has room to continue. Evolution Petroleum Q2 FY2026 earnings call highlights provided by user, covering dividend sustainability tension, EBITDA performance, and capital-light acquisition strategy. Alpha Vantage dividend history confirming 50-quarter streak, $0.12 per share consistency since Q3 2022, and full payout timeline back to 2013. Alpha Vantage cash flow statements providing annual and quarterly dividend coverage ratios and free cash flow analysis. Alpha Vantage earnings call transcript (Q4 FY2025) providing CEO and CFO commentary on capital allocation, commodity outlook, and acquisition strategy. You may think retirement is about picking the best stocks or ETFs and saving as much as possible, but you'd be wrong. After the release of a new retirement income report, wealthy Americans are rethinking their plans and realizing that even modest portfolios can be serious cash machines. Many are even learning they can retire earlier than expected. If you're thinking about retiring or know someone who is, take 5 minutes to learn more here.