yahoo Press

Global renewable energy installed capacity to double to 8.4TW by 2031

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

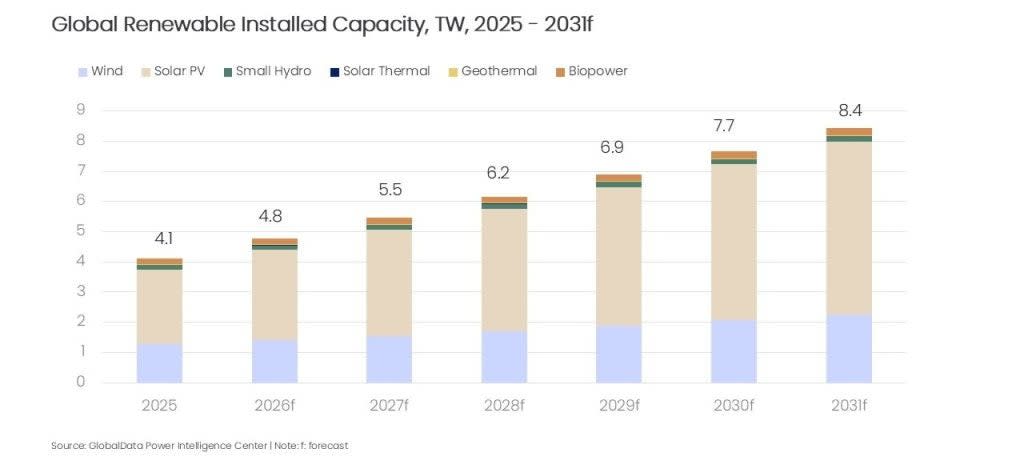

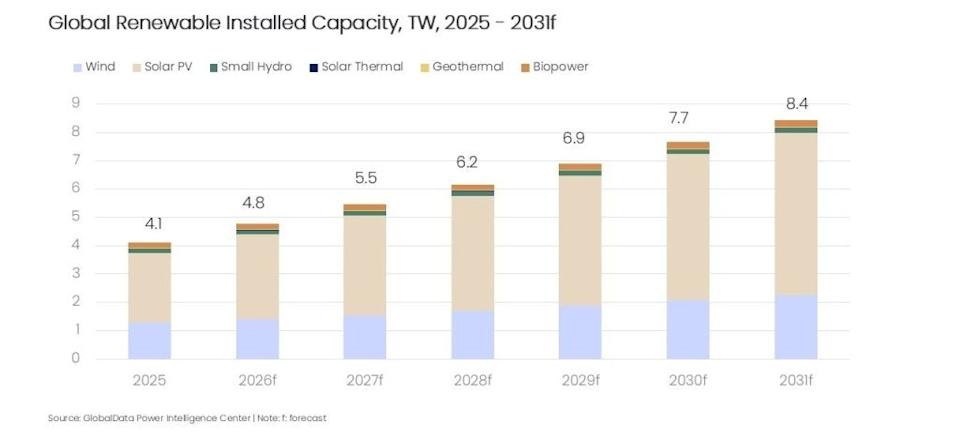

GlobalData’s latest report, 'Renewable Energy' is among the latest strategic intelligence reports from GlobalData, the industry analysis specialist. The report provides an industry analysis of the renewable energy market, its growing demand and how it is disrupting power utilities and the power sector. The report focuses on the trends related to renewable energy as a theme in technology, macroeconomic and regulatory trends. The report briefs on detailed analysis of the renewable energy value chain. The report is built as a single theme offering in-depth research using data and information sourced from industry associations, company websites, government websites, and statutory bodies. The information is also sourced through other secondary research sources such as industry and trade magazines. Global renewable energy installed capacity is set to expand at a rapid pace over the next five years, driven by the high scalability of solar PV deployment, persistent cost deflation, and increasingly robust policy tailwinds. Worldwide renewable installed capacity is forecast to more than double, from 4.1TW in 2025 to 8.4TW by 2031, registering a compound annual growth rate (CAGR) of 13% during the period. Worldwide renewable capacity reached a new peak in 2025, with the Asia–Pacific (APAC) region dominating wind installations at 699.5GW and solar PV capacity at 1,550GW, led by China. Across much of the world—again anchored by China—renewable investment and capacity additions continue to accelerate to record levels, while the US enters a phase defined by higher costs, increased volatility, and slower project delivery. Solar PV and wind will remain pivotal to the renewables transition globally. In 2025, solar PV emerged as the largest source of renewable electricity generation, surpassing wind. GlobalData estimates wind output at 2,770TWh in 2025, compared to 2,800TWh from solar PV. PV deployment in China is scaling rapidly, driven by carbon‑neutrality objectives, expansive investment throughout the supply chain, and sharp cost reductions that have positioned solar among the cheapest sources of electricity. China alone generated 1,150TW, accounting for around 41% of global solar PV output last year. The US and India followed, generating 486TWh and 189TWh, respectively. In both countries, solar PV output is rising rapidly, supported by steep cost reductions, increasingly enabling policy regimes—most notably the US Inflation Reduction Act and India’s flagship solar missions—and a strengthening imperative to decarbonise national power systems. In 2025, solar PV continued to dominate the global renewable capacity mix, accounting for roughly 56.1% of total installed capacity. Wind followed with a 33.5% share, while biopower represented 5.3%. AI is emerging as a pivotal, high-growth catalyst within the renewable energy sector, increasingly serving as the system’s “brain” to enhance efficiency, reliability, and profitability. Given the inherent intermittency of wind and solar generation, AI has become indispensable for ingesting and interpreting vast data streams, improving generation forecasting, optimising storage dispatch, and coordinating smart-grid operations. By enabling real-time balancing of supply and demand, AI reduces curtailment and operating costs while reinforcing overall grid resilience. Industry leaders such as Vestas, ENERCON, JinkoSolar, and First Solar are deploying AI at scale to boost operational performance, lower costs, and strengthen asset reliability. Data centres are emerging as a major, rapidly expanding, and strategically consequential driver in the renewable energy landscape, propelled largely by the surging electricity demand associated with AI workloads. In response, hyperscalers and colocation operators are accelerating investment in sustainable power solutions to meet rising loads while advancing decarbonization commitments. Technology firms are increasingly partnering with utilities and energy developers to lock in renewable supply for data centre operations, reflecting the scale and persistence of AI-led demand growth. For example, Google and NextEra Energy announced a collaboration in December 2025 to develop gigawatt-scale AI data centres powered by clean energy, while Equinix partnered with CleanMax on a 33MW captive renewable power project. After second-term policy shifts under President Donald Trump, renewable energy is entering a “two-speed” expansion: US federal support is tilting toward fossil fuels and away from green incentives, slowing deployment and raising costs, while the global transition continues, driven by falling costs, corporate demand, grid economics, and non‑US policies. By contrast, China’s clean-energy economy is accelerating. In 2025, clean energy drove over 90% of incremental investment growth, and renewable manufacturing and installation contributed more than a third of overall economic expansion. As a result, global renewables are increasingly decoupling from US federal policy, with the US facing slower rollout, while the rest of the world scales to record investment and capacity additions. "Global renewable energy installed capacity to double to 8.4TW by 2031" was originally created and published by Power Technology, a GlobalData owned brand. The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.