yahoo Press

SoundHound AI Expands Voice Platform Raises Questions On Core Infrastructure Role

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

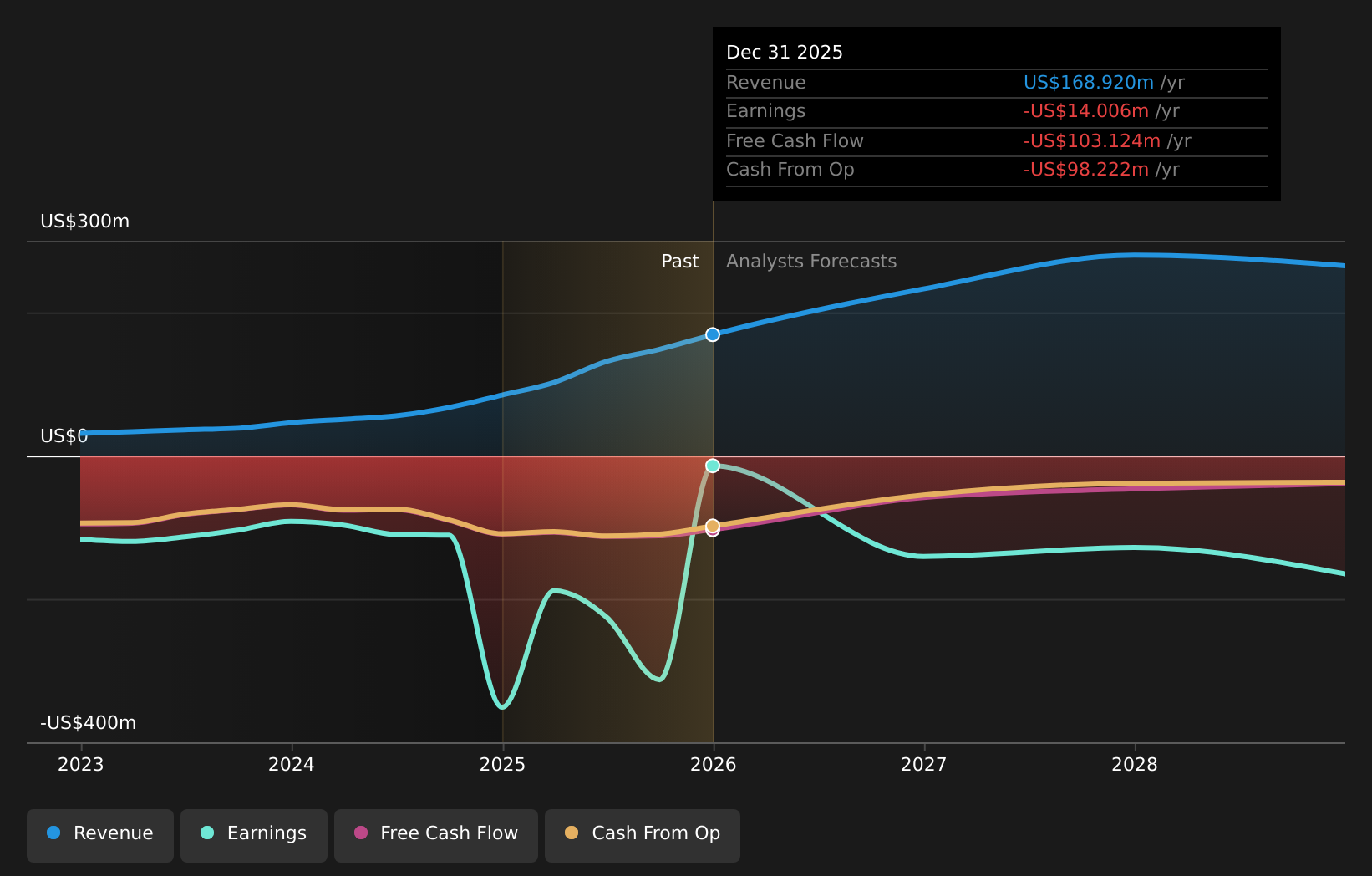

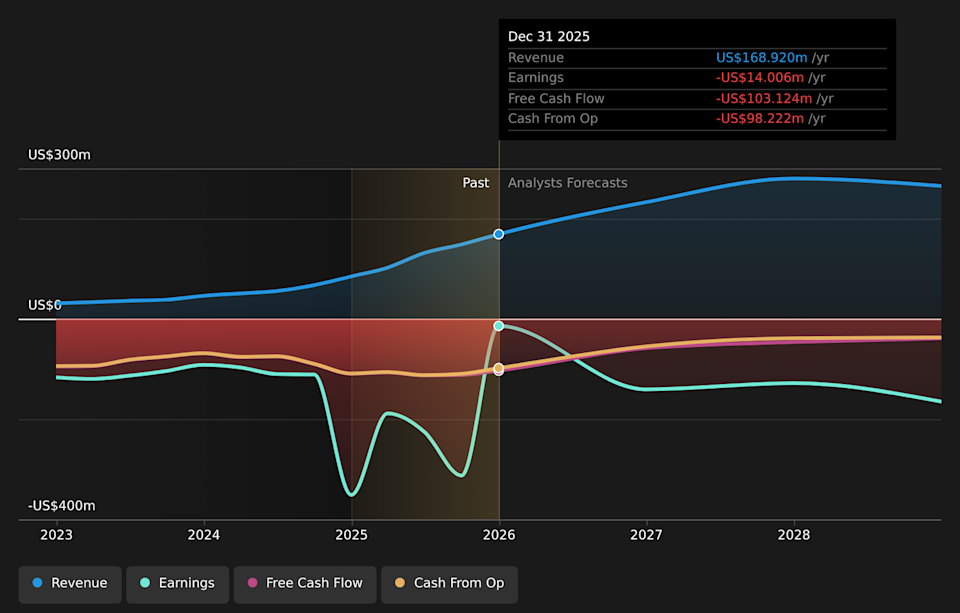

Find your next quality investment with Simply Wall St's easy and powerful screener, trusted by over 7 million individual investors worldwide. SoundHound AI (NasdaqGM:SOUN) has launched new voice-powered technologies aimed at retail, enterprise automation, and voice commerce. The move positions the company more directly in the broader AI economy by offering tools that could sit inside core business workflows. The launch has prompted discussion about whether SoundHound AI could become part of the underlying infrastructure for voice-driven AI services. With shares of SoundHound AI trading at $7.3, the stock has seen very large gains over three years, while more recent performance has been mixed. The share price is down 11.2% over the past week, 2.1% over the past month, 31.1% year to date, and 27.6% over the past year. This mix of strong multi year appreciation and recent weakness sets the backdrop for investors assessing what these new product moves might mean. For readers following the build out of the AI economy, this expansion into retail, enterprise automation, and voice commerce could mark a shift in how SoundHound AI is used across industries. The key question now is how quickly these new offerings gain traction with large customers and whether they become embedded in daily operations, potentially shaping how investors think about NasdaqGM:SOUN over time. Stay updated on the most important news stories for SoundHound AI by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on SoundHound AI. 1 thing going right for SoundHound AI that this headline doesn't cover. The push into retail, enterprise automation, and voice commerce effectively tries to turn SoundHound AI from a point-solution provider into a core workflow partner. If retailers, restaurants, and service providers start routing everyday tasks like ordering, customer support, and payments through SoundHound’s platform, that can deepen integrations and make contracts stickier. This sits on top of what is already a broad presence in automotive and customer service sectors, where the company has been winning deals against much larger players such as Amazon, Google, and Microsoft. At the same time, the business is still unprofitable, carries complex acquisition-related accounting, and relies on large enterprise contracts, so pushing deeper into the AI economy also increases execution risk. Investors weighing this news are essentially asking whether the company can scale usage and unit economics fast enough to justify building out what some see as voice infrastructure, while managing cash burn and intense competition from big tech and newer AI entrants. The new voice-powered tools directly align with the narrative’s focus on broader adoption across sectors like automotive, restaurants, and healthcare by pushing the platform further into everyday transactions and customer interactions. Rising spending on new products and verticals could challenge the narrative’s expectation of margin improvement toward near term profitability if revenue from these launches does not keep pace. The current narrative emphasizes partnerships and sector expansion, but may not fully capture how deeply voice commerce and in store retail agents could tie SoundHound AI into payment flows and data rich transactions. Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for SoundHound AI to help decide what it's worth to you. ⚠️ The company remains unprofitable, with analysts expecting earnings to decline on average over the next 3 years, so scaling these new offerings without tighter cost control could extend losses. ⚠️ Competition from large, well funded AI players and local providers in key markets may pressure pricing and make it harder for SoundHound AI to differentiate its voice solutions over time. 🎁 Revenue has been growing quickly, with sales nearly doubling from 2024 to 2025 and a 59% year on year increase in a recent quarter, showing clear client appetite for its voice AI platform. 🎁 Expansion into voice commerce, retail support, and enterprise automation adds more use cases on top of existing automotive and restaurant deals, which can broaden the customer base and recurring revenue potential. From here, pay close attention to how many large customers adopt these new voice-powered tools and whether they roll out across entire store networks or fleets, rather than staying in pilots. Contract wins, renewal rates, and the mix of transaction based versus fixed fees will help show if SoundHound AI is becoming embedded infrastructure or just one of many AI vendors. Investors should also track progress toward profitability, including trends in gross margin, operating expenses, and any further acquisition related charges, to see if growth is translating into a more sustainable business model. To ensure you're always in the loop on how the latest news impacts the investment narrative for SoundHound AI, head to the community page for SoundHound AI to never miss an update on the top community narratives. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Companies discussed in this article include SOUN. Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com