yahoo Press

US job growth seen moderating after robust January

Images

1 / 6

2 / 6

3 / 6

4 / 6

5 / 6

6 / 6

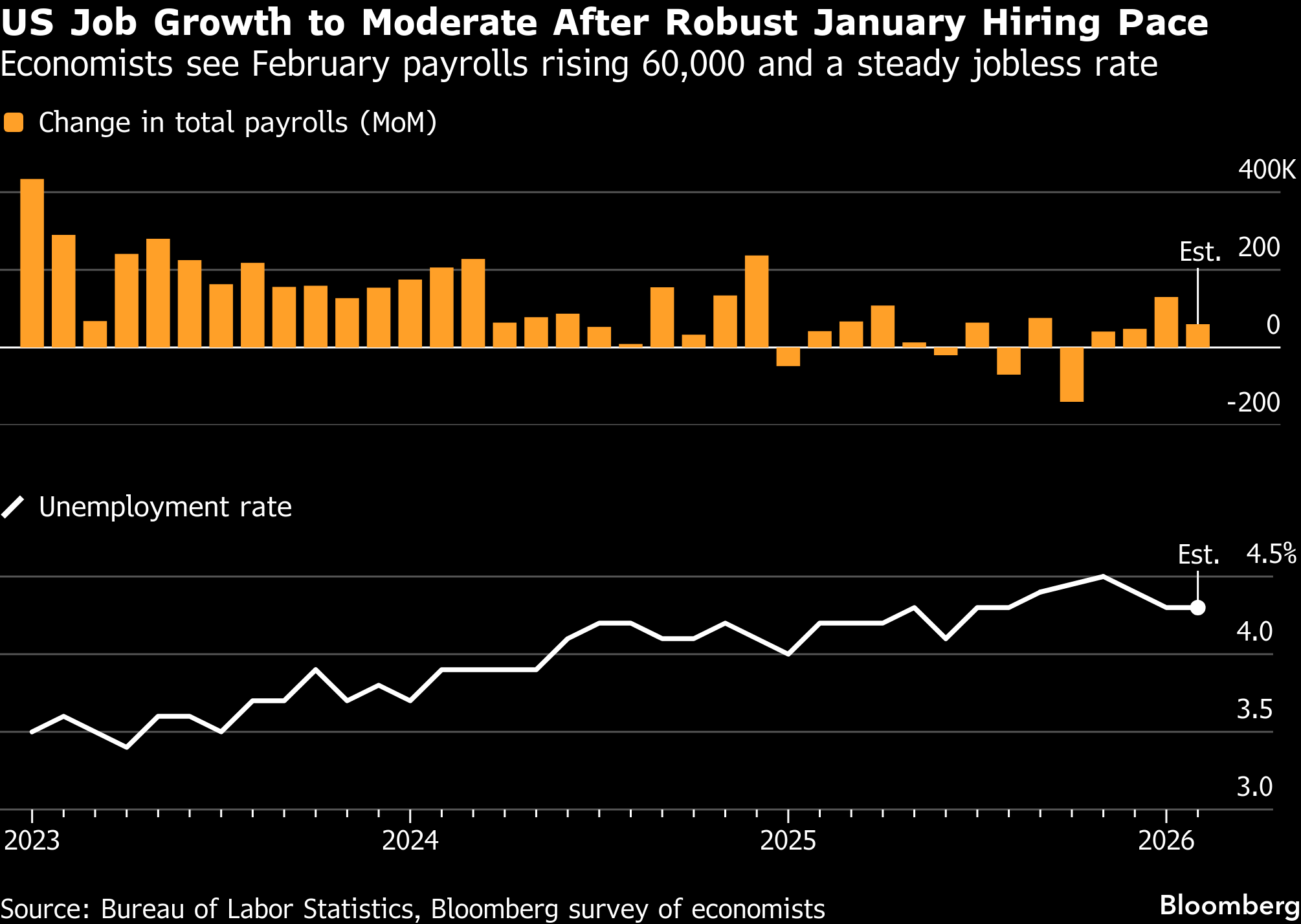

(Bloomberg) — US payrolls growth probably settled back in February after the strongest month of hiring in a year, returning to a more moderate and likely sustainable pace of hiring. Economists project 60,000 jobs were added for the month — less than half the number created at the start of the year, according the median of a Bloomberg survey ahead of Friday’s report. The jobless rate is seen holding steady at 4.3%. Most Read from Bloomberg Minneapolis Braces for Rent Crisis As ICE Surge Winds Down It’s a Tough Time To Be a Black Real Estate Developer New Tax Proposal Takes Aim at Thailand’s Salty Food Obsession Oslo Rebuilds Its Government Quarter with a New Focus: Openness Alberta’s Deficit To More Than Double, Hit by Oil Price Drop After years of scrambling to lure workers, employers dialed back hiring rapidly in 2025. The result was the weakest year for payrolls growth outside of a recession since 2003. That’s led to increased anxiety among American consumers who’ve been the primary source of fuel for the economy. The longer the job market limps along, the more consumer resilience will be put to the test. January retail sales data, due on the same day as the payrolls report, are unlikely to offer concrete signals either way because severe winter weather snarled activity across much of the US. Economists forecast a modest increase in receipts at US retailers other than auto dealers and gas stations. Fuel prices fell to a five-year low earlier in the month before rebounding in the closing weeks of January. Auto sales slumped, based on industry figures, also likely due to weather. “We expect a 30K drop in February payrolls, a sharp deceleration from January’s surprisingly strong print. The slowdown is more reflective of the cold spell in late-January and early February than a weakening in underlying hiring conditions. Weather-sensitive sectors were particularly hard hit, including construction and leisure and hospitality likely. But our broader takeaway is that labor market conditions have stabilized since last fall.” —Anna Wong, Stuart Paul, Eliza Winger, Chris G. Collins, Alex Tanzi and Troy Durie, economists. In addition to the jobs and retail sales reports, economists will parse a pair of surveys on manufacturing and services for clues about business sentiment. The Institute for Supply Management will issue its manufacturing index on Monday, followed by the group’s gauge of services activity on Wednesday. The Federal Reserve on Wednesday will release its Beige Book, offering anecdotal insight into economic conditions around the country. In Canada, officials will survey the outlook in a more shock-prone world, with Bank of Canada Governor Tiff Macklem discussing economic and financial stability risks and Deputy Governor Sharon Kozicki outlining how the monetary policy framework may need to adapt. Markets will also parse productivity data for signs that a rebound carried into year-end. Prime Minister Mark Carney is traveling to India, Australia and Japan, advancing efforts to diversify trade relationships. Elsewhere, a plethora of inflation numbers — from the euro zone to Turkey, and from South Korea to Chile — as well as multiple activity indexes and China’s National People’s Congress will be among the highlights. Fallout from joint US-Israeli strikes on Iran also will be in focus. The week kicked off with export data for South Korea, which showed an acceleration in February, reinforcing the central bank’s view that solid semiconductor demand is helping cushion the economy as it maintains a neutral policy stance. Australia releases data Wednesday that’s expected to show that growth picked up a tad in the fourth quarter, in figures likely to sustain speculation over another Reserve Bank of Australia rate hike this year after January inflation held above the bank’s target. China gets PMI statistics the same day that will probably highlight the need for more policy support after a sluggish start to the year. Meanwhile, the National People’s Congress that starts on Thursday will set the tone for the economy in the year ahead. Official manufacturing and non-manufacturing gauges for February are both forecast to stay contractionary. The RatingDog indexes also due have tended to be a little more upbeat. Other Asian nations releasing PMI statistics in the coming week include Indonesia, Malaysia, the Philippines, Thailand, Singapore, South Korea, Taiwan and Vietnam. Japan’s Ministry of Finance on Tuesday releases a report card for corporations. Fourth-quarter profits will give an indication of whether firms have scope to maintain robust wage growth, and capex data will be watched closely after preliminary GDP for the period showed anemic 0.2% growth in business spending. Tuesday’s figures will be factored into revised GDP due March 9. South Korea’s consumer inflation is seen picking up a bit in February, to 2.2%, likely keeping the Bank of Korea in a holding pattern for now. Indonesia’s February consumer inflation is expected to accelerate to 4.34% after recording the fastest clip since 2023 a month earlier, in data that could test Bank Indonesia’s resolve to stay accommodative. Also releasing CPI figures are Thailand, the Philippines and Vietnam. Trade data are due from Vietnam, Australia, Indonesia and Pakistan. In central bank action, three RBA officials are due to speak, possibly offering clues on the timing of the next rate hike, with pricing in the overnight-indexed swaps market implying only the sliver of a chance of a back-to-back increase at the next decision on March 17. Assistant Governor Sarah Hunter speaks at the Norges Bank Conference in Oslo on Monday. The following day, Governor Michele Bullock delivers a speech at the AFR Business Summit in Sydney, and Deputy Governor Andrew Hauser speaks on a panel in New York at the end of the week. Elsewhere, Malaysia’s central bank is forecast to hold its overnight policy rate steady at 2.75% on Thursday. It’s a big week for inflation. After mixed reports from three of the euro area’s largest economies, forecasters anticipate overall annual consumer-price growth at 1.7% in February. That would match the prior reading, which was the lowest since September 2024. Those data on Tuesday will be released concurrently with Italy’s inflation number, which is expected to show a slight uptick, to 1.1%. Other euro-zone statistics include industrial production in France and Spain on Thursday, offering the first solid glimpses of manufacturing at the start of the year. German factory orders on Friday may similarly illustrate if Berlin’s defense and infrastructure stimulus is feeding through to the region’s largest economy. Among several European Central Bank events on the calendar, President Christine Lagarde will make appearances on Monday and Thursday, while Executive Board member Isabel Schnabel speaks in New York at the end of the week. Speaking on Sunday, Bundesbank President Joachim Nagel said the current “inflation picture in the euro area is favorable overall” and that “we are in a good position” on monetary policy. Potential sovereign credit assessments after the market close on Friday include France and Portugal at Fitch Ratings. The main UK focus will be Chancellor Rachel Reeves’ Spring Forecast on Tuesday. Expectations are muted, though the backdrop of political turmoil around Prime Minister Keir Starmer’s leadership may draw attention to any fiscal implications. In Sweden, the CPIF measure of consumer prices targeted by the Riksbank may have dropped to 1.8% in February, its lowest since 2024. Core inflation probably slowed too, undershooting the central bank’s forecasts, in part because of a stronger currency. Those numbers are due on Thursday. Equivalent data will come out in Switzerland on Wednesday. Most economists reckon inflation either stalled or prices showed outright annual declines last month. While that will throw focus on the Swiss National Bank, President Martin Schlegel, already acknowledged the possibility of “negative prints” while insisting such outcomes wouldn’t be a problem. Turning to Eastern Europe, Hungary’s fourth-quarter growth data on Tuesday will offer clues on whether a pre-election upswing Prime Minister Viktor Orban is banking on has materialized. Romania, meanwhile, is expected to deliver a draft budget for 2026. On Wednesday, Poland’s central bank may resume rate cuts, with inflation projected to stay low. Finally, Turkish data on Tuesday may show inflation accelerated to 31.5%. Officials have largely attributed the rise in prices to food costs and described it as temporary. Rate cuts are expected to continue, though possibly at a slower pace than January’s 100 basis-point reduction. Chile on Monday posts January GDP-proxy data, likely buoyed by domestic demand, near record prices for copper — the country’s No. 1 export — and high expectations for market-friendly policies from President-elect Jose Antonio Kast. Later in the week, February inflation data out of Chile is expected to show a month-on-month cooling from January’s 0.4%, pushing the year-on-year reading to roughly 2.5% — the slowest pace since August 2020. Banco Central del Uruguay on Tuesday is slated to meet after delivering a 100 basis-point cut, to 6.5%, in January. Uruguay also serves up February inflation readings, which have slowed for three straight months to a below-target 3.46%. The main event from Brazil is fourth-quarter and final 2025 output results, expected to again highlight the drag on Latin America’s No. 1 economy from the central bank’s uncompromising monetary policy. Year-on-year readings will likely come in just below the third-quarter’s 1.8% print, while economists see 2025 full year growth having downshifted to roughly 2.3% from 3.4% in 2024, which would be the lowest since 2020’s -3.3% pandemic-induced slump. Brazil also reports industrial production and the national unemployment rate, which hit a record-low 5.1% in December. Closing out the week is Colombia’s inflation, which likely drifted higher from January’s slightly-less-than expected jump to 5.35%. A 23% minimum wage hike that was suspended by the high court in mid-February and restored by decree less than a week later has thoroughly roiled expectations and analyst estimates. —With assistance from Charlie Duxbury, Beril Akman, Brian Fowler, Laura Dhillon Kane, Monique Vanek, Piotr Skolimowski, Robert Jameson and Mark Evans. Most Read from Bloomberg Businessweek Claude Code and the Great Productivity Panic of 2026 How Covid Quietly Rewires the Brain The Buyers Behind Gold’s $5,000 Breakthrough America’s Love of Ube Is Straining Supplies in the Philippines Indian Desserts Are Ready for Their Matcha Moment ©2026 Bloomberg L.P.