yahoo Press

Micron’s Early HBM4 Ramp Tests Durability Of AI Memory Boom

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

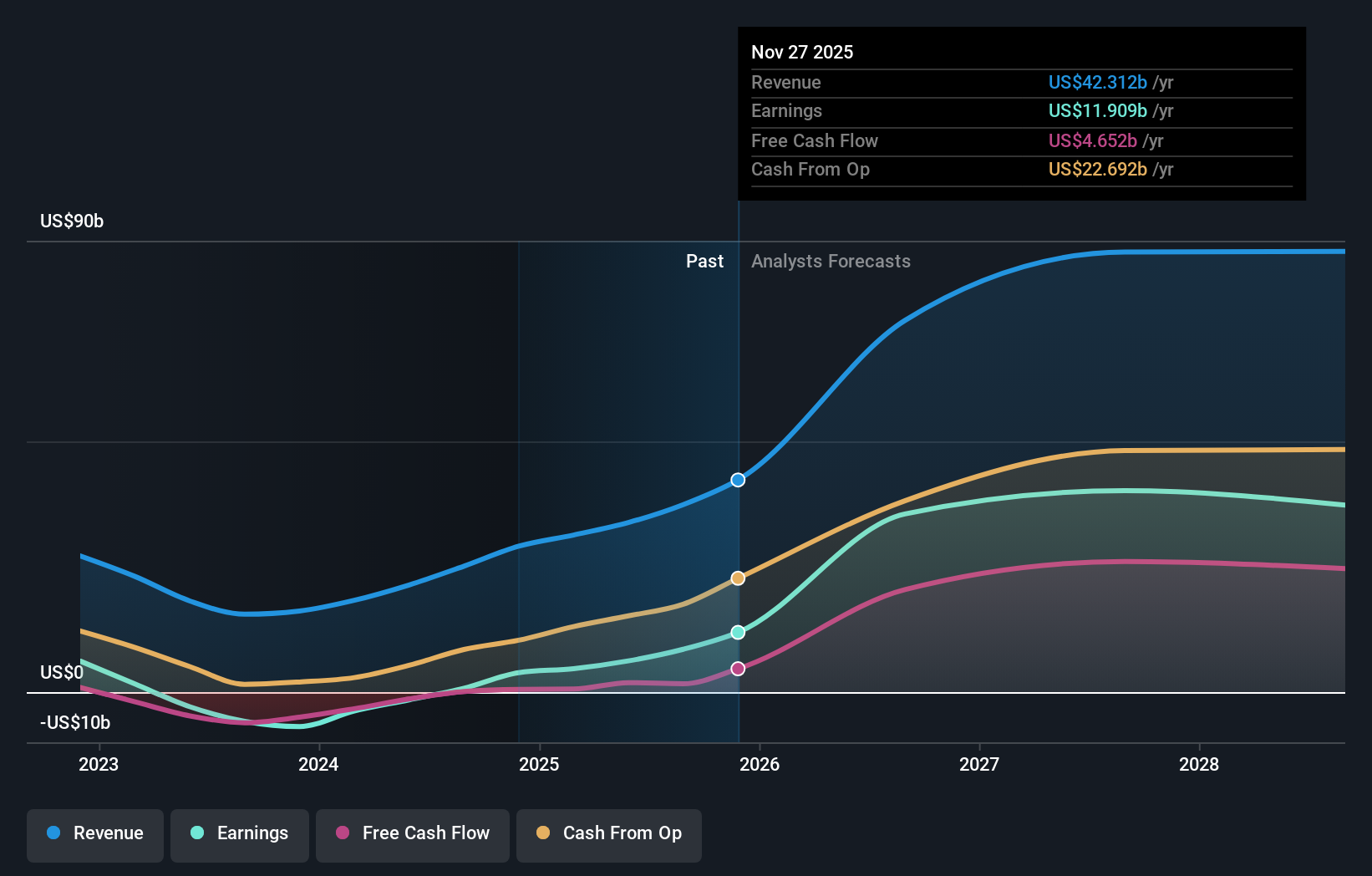

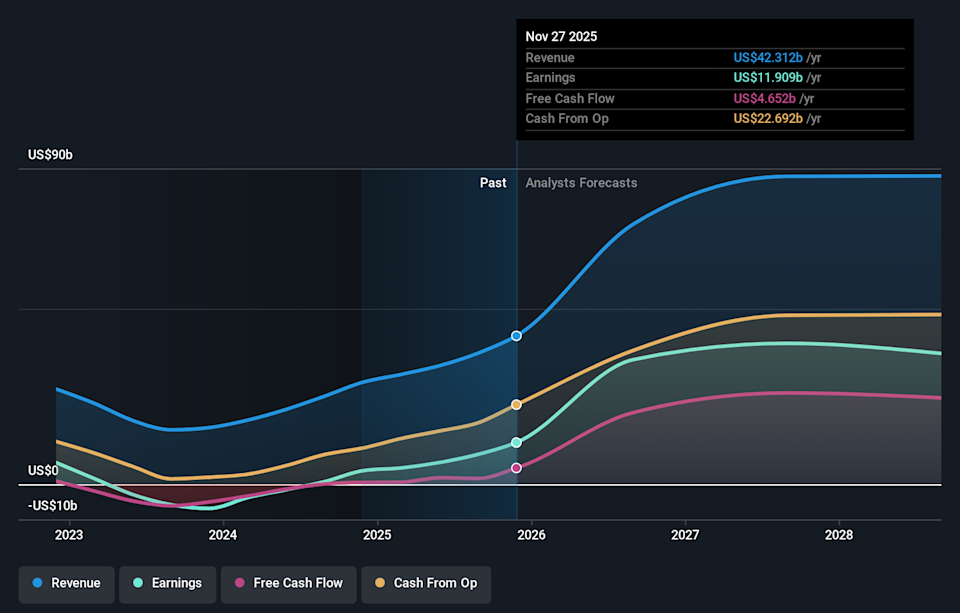

Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE. Micron Technology, ticker NasdaqGS:MU, has begun high volume production and ahead of schedule shipments of its HBM4 memory chips. The company reports that all of its 2026 HBM supply is already committed, reflecting very strong interest from hyperscale and AI customers. Samsung is accelerating its own HBM4 rollout, increasing competitive pressure in high bandwidth memory. Micron is stepping directly into the center of the AI infrastructure buildout with this early HBM4 ramp, and that context helps explain why the stock has attracted attention. Shares recently traded at $411.66, with gains of 4.3% over the past week and 23.5% over the past month. The move over the past year has been very large, and the 3 year return of about 7x highlights how central investors now see Micron in high performance memory. For you as an investor, the key question is how sustainably Micron can turn this HBM4 momentum into long term earnings power while Samsung and others push to catch up. The company’s sold out 2026 HBM capacity points to strong demand visibility, but future returns will depend on execution, pricing, and how the competitive race plays out in high bandwidth memory. Stay updated on the most important news stories for Micron Technology by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Micron Technology. We've flagged 1 risk for Micron Technology. See which could impact your investment. Micron’s quarter-early HBM4 ramp and sold out 2026 supply put it firmly in the thick of the AI data center buildout. For you, the key takeaway is that Micron is not just shipping volume, it is shipping one of the highest value products in its portfolio into a market that analysts describe as supply constrained. That can support pricing and margins as long as HBM supply tightness persists. At the same time, Samsung and SK Hynix are racing to qualify and scale their own HBM4 lines, so the current shortage could ease if all three push capacity aggressively. The early ramp also comes with heavy capital spending commitments in the U.S. and Asia, which can pay off if utilization stays high but can weigh on returns if demand normalizes. The early HBM4 production ramp supports the narrative that AI and data center demand are pulling Micron further into high value memory, with tighter supply conditions helping pricing and margin expansion. Rising competition from Samsung and SK Hynix directly challenges the thesis that Micron can enjoy sustained pricing power, because additional high bandwidth memory capacity may compress margins over time. The intensity of current HBM shortages and the speed of Samsung’s HBM4 ramp introduce an extra layer of supply cycle risk that is not fully captured by a simple AI driven growth story. Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Micron Technology to help decide what it's worth to you. ⚠️ Additional HBM4 supply from Samsung and SK Hynix could ease today’s shortage and put pressure on high bandwidth memory pricing, affecting Micron’s earnings power. ⚠️ Large capital spending on HBM and new fabs raises the risk that returns fall if AI infrastructure spending or memory pricing soften from current levels. 🎁 Micron’s HBM4 supply being sold out through 2026 gives unusual multi year visibility in a segment that is currently in short supply, supporting revenue and margin potential. 🎁 Tight memory markets tied to AI data centers give Micron leverage in high bandwidth and advanced DRAM products, which analysts already link to stronger profitability and earnings growth. From here, you may want to watch three things closely. First, how fast Micron can scale HBM4 volumes while keeping yields and quality where hyperscale customers need them. Second, announcements from Nvidia, Samsung and SK Hynix about HBM4 qualifications and purchase allocations, which will signal how share is splitting across suppliers. Third, Micron’s own updates on capital spending, pricing trends and contract lengths for HBM and advanced DRAM, because those details will show whether today’s shortage is translating into durable earnings rather than just a short, sharp upcycle. To ensure you're always in the loop on how the latest news impacts the investment narrative for Micron Technology, head to the community page for Micron Technology to never miss an update on the top community narratives. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Companies discussed in this article include MU. Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com